We believe accountability and modesty are among the keys to success in this business. In striving for those qualities, LPL Research has a tradition of starting off a new year with a lessons learned commentary. We got some things wrong last year, no doubt. But those who don’t learn from their mistakes are doomed to repeat them. Here are some of our lessons learned from 2022. As you might imagine, inflation and the Federal Reserve are common themes throughout.

Lessons learned: Economic forecasts

The Fed’s bark was as bad as its bite!

Investors have been carefully dissecting Federal Reserve (Fed) officials’ words for decades, and depending on the composition of the Federal Open Market Committee (FOMC), its bark is often worse than its bite. But this time was probably different. One of the lessons learned in 2022 was to never underestimate our central bank’s resolve to squelch inflation. Another corresponding teachable moment was never overestimate the speed of price declines.

At the start of 2022, markets expected the upper bound of the fed funds rate to stay below 1%. The expectation was predicated on the view that inflation pressures would ease as global economies recalibrated to a post-pandemic environment. But inflation was stickier than anyone anticipated, and the inflation dynamics were further exacerbated by Russia’s invasion of Ukraine and COVID-19-related lockdowns in China. As inflation accelerated in early 2022, especially housing prices, members of the FOMC started warning investors about the need for aggressive action to fight inflation.

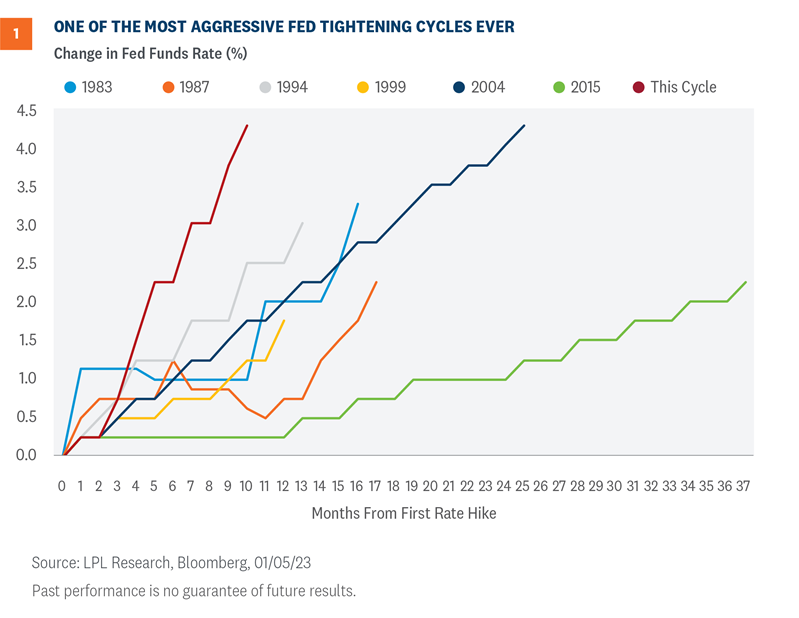

As shown in Figure 1, policy response was as aggressive as policymakers’ speeches. Policy makers were more intent on tightening financial conditions than virtually anyone anticipated. Investors have never seen four consecutive 75 basis point (0.75%) rate increases by the FOMC since the Fed started explicitly targeting the fed funds rate to implement monetary policy.

These lessons learned from 2022 are particularly important for 2023 since FOMC members expect rates in 12 months to be higher than what investors are currently expecting. Caveat emptor.

Lessons learned: Equity Market forecasts

Stock market impact from gradual hikes is very different than impact from steep hikes

Entering 2022, the LPL Research team agreed with the Fed that there was a path to a soft landing, despite high inflation. A soft landing is still possible at this point, but the path has narrowed a lot over the past six months or so given the aggressive Fed response to last year’s inflation surge.

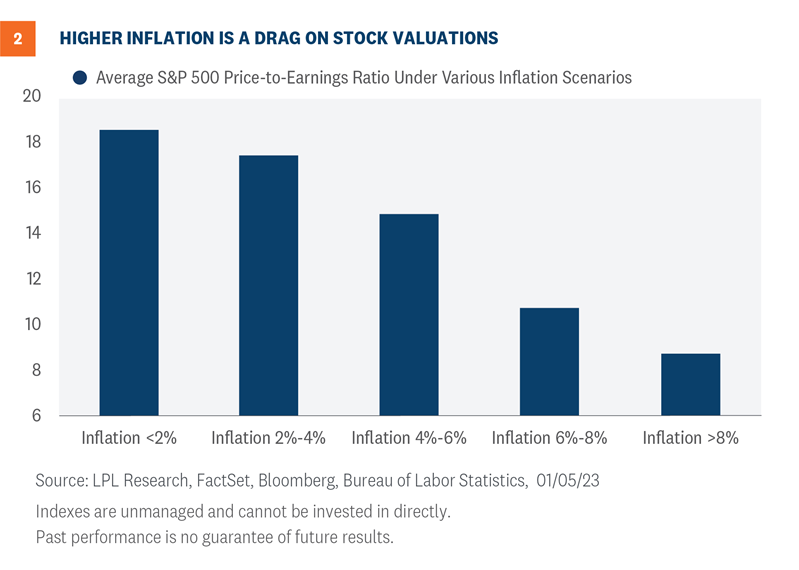

When LPL Research released the Outlook 2022: Passing the Baton in December 2021, the team’s view was that the hit from inflation would be manageable and would therefore limit the number and magnitude of interest rate increases, enable the U.S. economy to avoid recession, and support above-average valuations. Well, the hit from inflation was worse than we anticipated, the Fed was surprisingly aggressive (central bankers were clearly too slow in recognizing the severity of the inflation problem), and interest rates spiked well above our initial forecast. The relationship between inflation and stock valuations is a strong one, as shown in Figure 2, which meant the market could no longer support price-to-earnings (P/E) ratios over 20 (the same goes for the relationship between interest rates and stock valuations). The hit to valuations in the form of about 4 P/E points (21 to 17) translates into a roughly 20% drop in the S&P 500 Index.

While our team underestimated inflation and the resulting hit to valuations last year, there were some wins. LPL Research’s $220 S&P 500 earnings per share forecast at the start of the year looks spot on—consensus is now calling for $220.30 for 2022, with the fourth quarter yet to be reported. And on the asset allocation side, the team’s preference for value stocks throughout the year turned out to be a win.

Lessons learned: Bond Market forecasts

Relying on history doesn’t always work

Coming into 2022, we had the expectation that interest rates would rise from very low levels, but we thought the rise in rates would be gradual. At the start of the year, we assumed the Fed would take a gradual approach to removing the very accommodative monetary policy that had been in place, frankly, since the end of the global financial crisis. The reason? The last few rate hiking campaigns were very slow and deliberate. If you look back at the rate hiking campaign that began in 2015, for example, the Fed raised interest rates by 0.25% in December 2015 and didn’t hike rates again until December 2016. Moreover, if you look at the rate hiking campaign that began in 2004, the Fed didn’t actually get to its terminal rate until 2006—a full two years after it started. However, what transpired over the course of 2022 turned out to be the most aggressive rate hiking campaign in four decades.

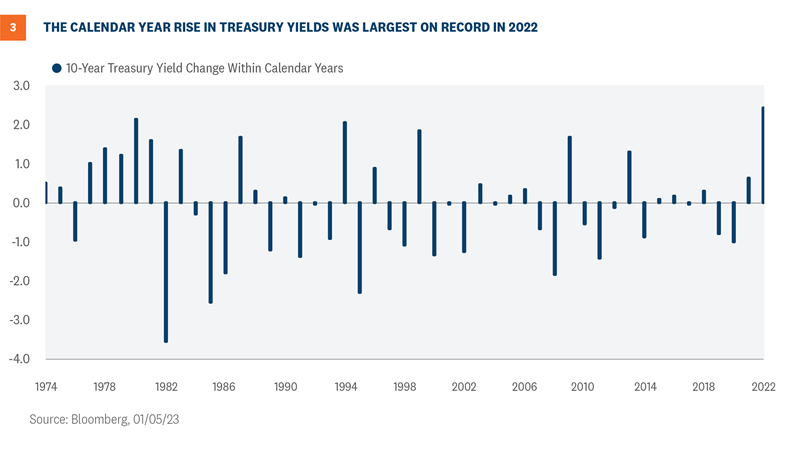

Because of that aggressive rate hiking campaign that took place largely in one calendar year, we saw Treasury yields increase the most in one calendar year on record. The chart below shows the changes in the 10-year Treasury yield on a calendar basis and the 2.4% increase in yield last year was more than any calendar year period on record; even during the 1970s and 1980s when interest rates were significantly higher than today. That upward pressure on yields certainly caused fixed rate coupon paying bonds to sell off dramatically last year, resulting in the worst year on record for core bonds (as measured by the Bloomberg Aggregate Bond Index).

Conclusion

LPL Research had some hits and misses in 2022, no doubt. As always, we try to learn from the misses while still recognizing the hits. After underestimating the inflation surge last year, the Fed and markets may be erring on the other side this year. The forces now pushing down on inflation are getting stronger, which may keep interest rates down and stock valuations supported this year. Here’s hoping for more hits and fewer misses for all of us in 2023.

Jeffrey Buchbinder, CFA, Chief Equity Strategist, LPL Financial

Lawrence Gillum, CFA, Fixed Income Strategist, LPL Financial

Jeffrey Roach, PhD, Chief Economist, LPL Financial