Many pundits are issuing recession warnings and saying the economy is heading for a hard landing. Amid the cacophony of voices, we think the economy is slowing just like central bankers want but not shrinking. Further, we argue that a slowing economy is very different than a shrinking one.

Economy Slowing, Not Shrinking

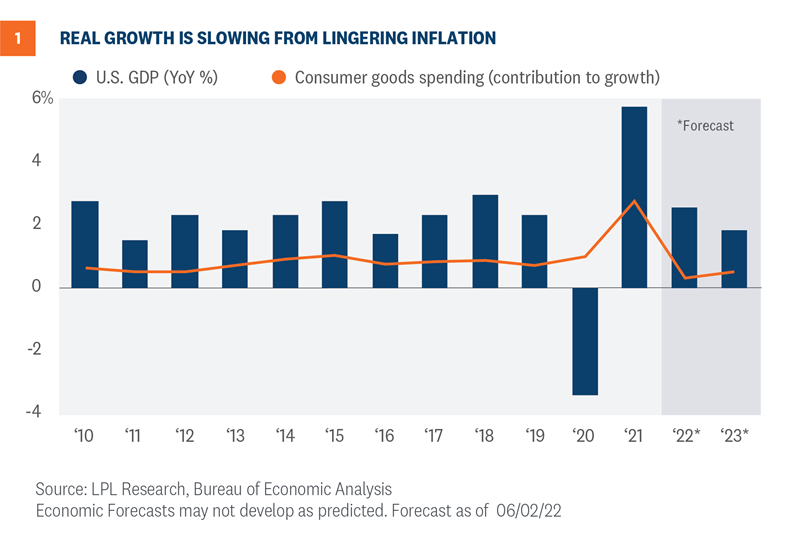

We believe the domestic economy will continue to grow this year. Other than the GDP (gross domestic product) anomaly in Q1, we think the economy has sufficient momentum to offset the inflationary pressures. “Our base case forecast is an inflation rate that moderates as supply bottlenecks improve and we get some closure to the Russian war with Ukraine,” explained LPL Financial Chief Economist Jeffrey Roach. Figure 1 shows our most likely scenario: the economy avoids a recession as forecasted growth approaches 2.6% in 2022 with another downshift to under 2% in 2023.

The U.S. economy grew 5.7% in 2021 after contracting by 3.4% the previous year. Last year consumer spending was extremely robust, particularly on consumer goods as consumers were still less inclined to spend on services. Goods spending contributed roughly 2.7 percentage points to the headline growth rate, the highest since 1955. While we do not think consumer spending will continue at this clip in 2022, the consumer will likely weather the headwinds of high prices and geopolitical uncertainty and support the overall economy throughout 2022.

Consumer spending will likely slow the latter half of this year as inflation pressures weigh on consumers and wage growth likely lags inflation. These factors in tandem will erode consumers’ real purchasing power. However, recent spending activity shows a fairly stable consumer. Real consumer spending rose 0.7% in April, the fourth consecutive monthly increase in real spending. The job market is tight, supporting consumer spending from gains in personal income, but the real cushion for consumers comes from roughly $3 trillion in excess savings accumulated during the pandemic.

Inventory Rebuilding Could Add to Growth

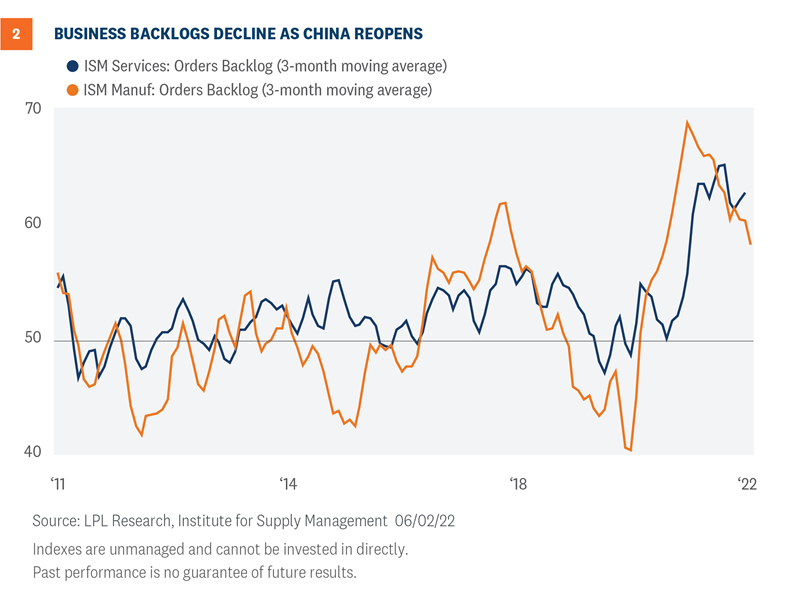

If supply bottlenecks improve, we expect to see firms restocking inventories, supporting underlying economic growth. As shown in Figure 2, the latest reports from the Institute of Supply Management show that order backlogs are declining for both the manufacturing and services sectors. As firms have improved access to required inputs and as the transportation sector recalibrates to the current environment, the economy could likely see growth in the latter half of this year and avert recession.

Inflation Is Still the Wild Card

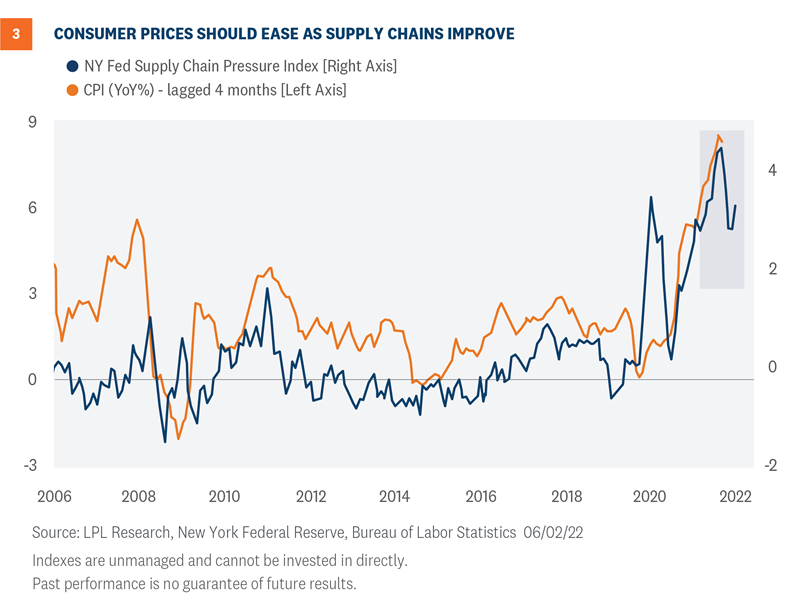

Inflation will still likely be above the Federal Reserve’s (Fed) long-run target, but inflation growth rates will likely cool throughout this year. As shown in Figure 3, improvements in supply chains impacted consumer prices. Technically, consumer price changes lagged four months and are 72% correlated with the New York Fed’s Global Supply Chain Pressure Gauge. Given the improvement in supply chains, inflation pressures should subside. And as inflation eases, the Fed will not likely need to increase rates much above neutral.

Residential Investment Will Put a Drag on Growth in the Second Half

A slowdown in residential investment will likely have a big impact on growth this year. The slowdown could come from both the demand and supply side as interest rates increase. The average rate on a 30-year fixed rate mortgage rose over 2 percentage points since the beginning of the year and has created a damper on housing activity. Secondary effects from rising mortgage rates will likely slow consumer spending. At the beginning of this year, the principal and interest payment on a $300,000 loan at 3.27% was $1,309. At the end of May, the monthly payment rose by $366. As housing becomes a larger percentage of an individual’s budget, we will likely see a decrease in discretionary spending.

When we look at changes in borrowing costs we often focus on homebuyers, but higher borrowing costs also affect builders. High capital and labor costs are a current challenge for all builders, and high interest rates particularly impact developers who rely on the debt market for construction. Tighter financial conditions could eventually slow new home construction, putting a damper on home supply and residential investment. Inventories of new and existing homes are already low, and if builders slow the rate of construction, home prices will not likely decline as much as they did in 2006 – 2011 since current supply is low.

Risks to the Outlook

A still unknown variable to our forecasts is the Federal Reserve’s shrinkage of its balance sheet, known as quantitative tightening (QT). The Fed will only allow its balance sheet to shrink incrementally over time while also paying attention to the impact QT is having on the markets. The Fed has stated that QT could “replace” several rate hikes as a way to tighten financial conditions; therefore, we could conceivably see a lower fed funds terminal rate than what is already priced in the markets, which should help the Fed navigate a “softish” landing of the economy slowing but not shrinking.

Jeffrey Roach, PhD, Chief Economist, LPL Financial

Lawrence Gillum, CFA, Fixed Income Strategist, LPL Financial

______________________________________________________________________________________________

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered inv estment advisor and broker -dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment a dvice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value